M&A in the Gaming Industry

Covid-19 impact on the industry

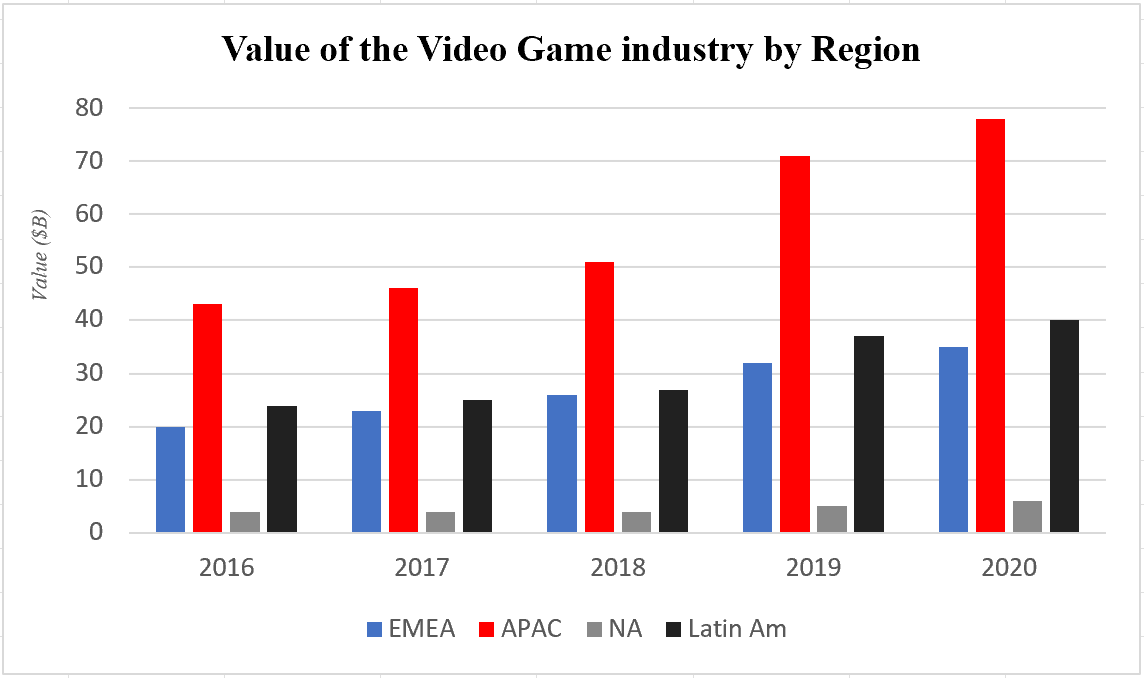

The Covid-19 pandemic dumped many sectors such as tourism, whose global revenue was cut in half in 2020, or the airline industry with an RPM waning by 80%. But, just like in every crisis, there are also a bunch of winners. This is the case of Amazon, with a revenue growth of 38%, with an almost doubling net cash generated from operating activities ($38,514m in 2019 to $66,064m in 2020). Both positive and negative impacts were caused by fears and government restrictions, leading to lockdowns. With an increasing time spent at home, people ordered more online but also played more, which translated into a booming gaming sector. This way the Video Gaming industry topped at $175 billion in 2020, a 10% increase from 2019. This growth mostly came from Asia, and mobile gaming, especially in China.

Source: Wepc (Jan 2022)

Benefiting from high margins, due to very few variable costs, companies generated a lot of cash. For example, Nintendo generated a net income growth of 36.28% in 2020 and 89.77% in 2021. This cash was quickly reinvested in external growth initiatives because of the competitive market. They turned to M&A more than ever, with a number of operations in Q1 2021 superior than in the whole 2020. This drove record level of valuation with multiples never attained since the dot com bubble of 2000, like with the Glu Mobile’s acquisition by Electronic Arts for $2.1b, and an EV/EBIT multiple of 24.2.

Synergies

The first interested in these operations were the industry companies themselves, because they live in an industry very prone to synergies. A company can simply acquire another just to gain a revenue growth that’d instantly boost valuation, but buying a company can also mean gain complementarity for certain types of products, and cost reductions, especially from the economy of scale. The real synergy came from the vertical integration of other types of companies involved in the development of a game. Companies are originally either studios, charged of the game conception, editors, charged of the marketing and commercialization, or consoles companies, charged of the material manufacturing. We can look at the examples of Microsoft, originally a console company, which acquired the studio ZerniMax Media early 2022 for $7.5B, and Ubisoft, originally an editor, which acquired many studios developing mobile games. This led to an +35% increase in 2020’s number of transactions in a sector in which they were stagnant.

Cloud gaming and GAFAMs

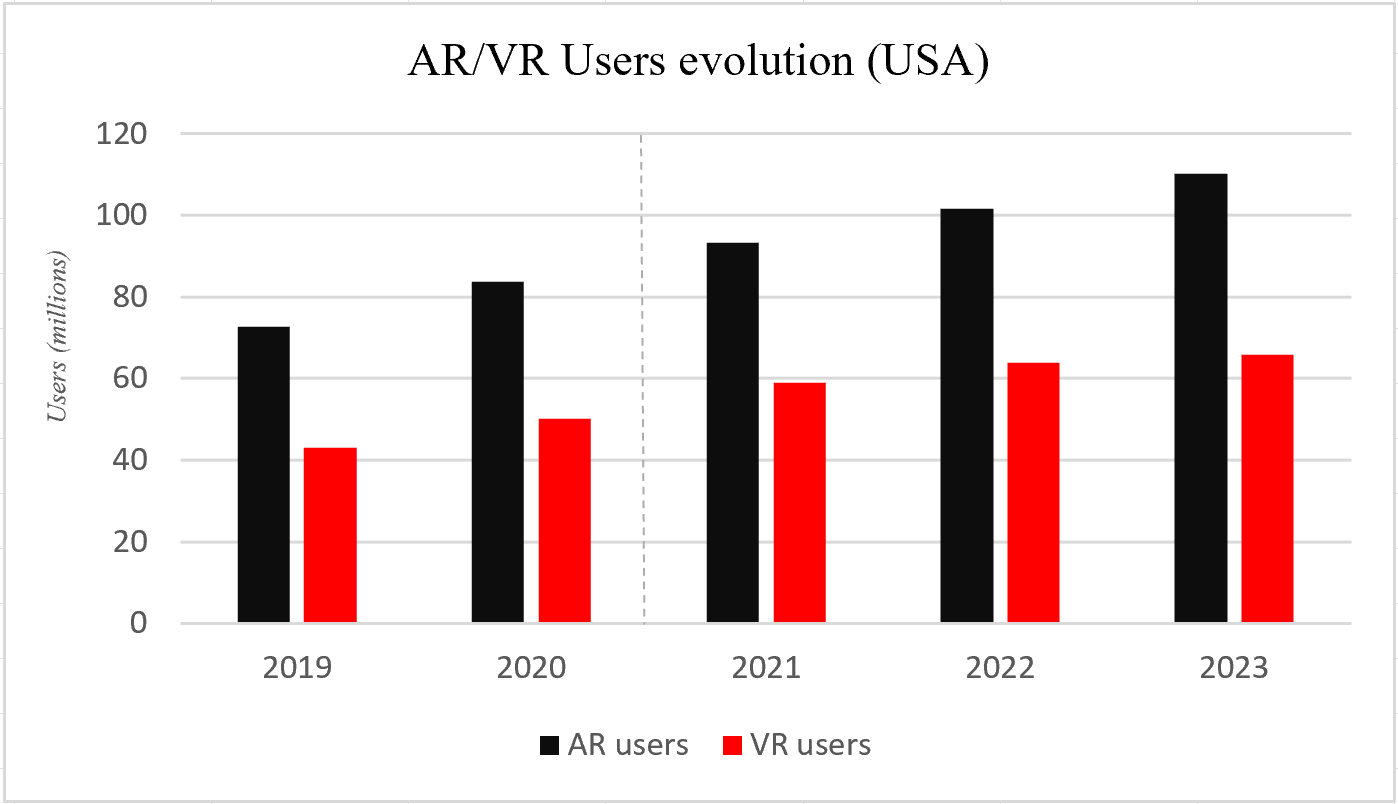

We already said the social distance due to the pandemic benefited the VG industry, but not only. This also fostered the ongoing evolution of video games into social platforms. Extended Reality and Virtual Reality (XR and VR) use changed from only fun to a place for social interactions, with the number of users growing by 14% growth in 2020.

Source: eMarketer (March 2021)

Other tech companies, like GAFAM, are interested in this technology, and in the overall sector. For the last five years, they have been investing their ridiculously high profits in divertissement. This began with Apple TV+ and Amazon Prime video. Facebook had also bought the Occulus VR in 2014 for $2b and is investing records amounts in the metaverse ($10b a year). They are now all turning to cloud gaming. With a number of players that should grow to 3b in 2023, they saw the opportunity and forecasts are now saying cloud gaming technology should represent $6.5b in 2024 against $1.5b now. To illustrate, Netflix acquired Night School Studio in September 2021 and Amazon developed its own cloud gaming service (Luna), which will be proposed in monthly subscriptions or bundles, without the gaming normal constraints.

Now that they are all proposing these services, the goal for the giants is to acquire as many licenses as possible. That is actually the reason why 9 out of 10 of the sectors’ acquisitions are studios. Facebook gaming and Microsoft cloud acquired PlayGiga ($70m) and Zenimax (8 studios for $8.1b) to garnish their offer. These are very targetted acquisitions, by adding to their platform Disney, Warner Bros, and Sega games, they assure themselves a part of the market. Moreover, the development of 5G over the world is closely tied to cloud gaming, as its number 1 purpose is to offer players the ability to play anywhere, anytime.

An opportunity for Private Equity

But they are not the only ones to recently invest massively in the VG industry, Private Equity firms are doing the same, but for other reasons. First, remembering their purpose is to buy and resell a company later, at a higher valuation, almost all other sectors are offering less growth potential and more downside possibilities. Furthermore, if the covid-19 pandemic restarts as we can see in China, they have a lot to lose in the traditional industries, and prefer taking as less risks as possible.

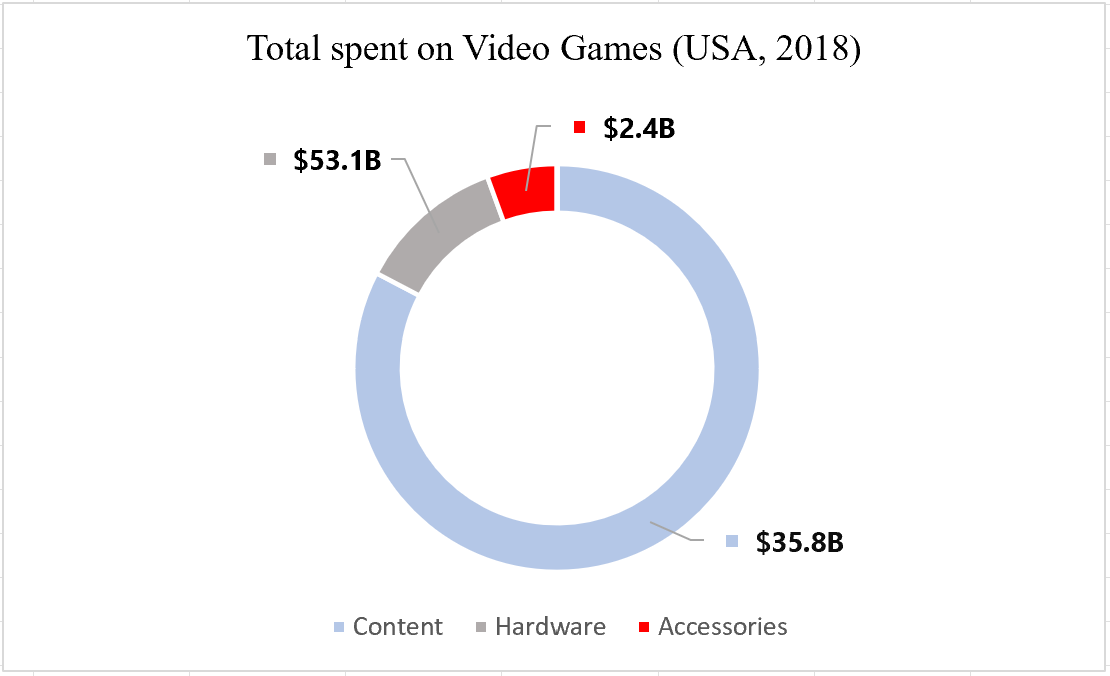

This new interest is also related to the new ways to generate money that were not exploited before. At the time, customers bought the game and that was it. Today, you can transform free-to-play games into real cash-generating machines. You can add monthly subscriptions that were popularised by World of Warcraft, forcing the player to buy it to get the full content. You can also sell skins only acquirable through real money, like in Riot’s League of legends, or simply add costly updates (DLC) to your games like EA sports. To give some perspective, EA generated $5.6b in 2021 for an EBIT of $1b.

Source: The ESA, The NPD Group (2019)

Just like other internet companies, once well established, few are the costs compared to the massive profits. This way, with a predicted 9% annual growth for a $176bn market, P.E. companies, like Carlyle Groupe are investing big-time amounts. Early 2021, the firm bought the editor company Jagex for $530m in early 2021. Precisely, Venture Capitalist Firms are investing in early-stage companies in the sector, which are approximated to be 65% of the sector’s deals, for a value of $1.1b.

A bright horizon

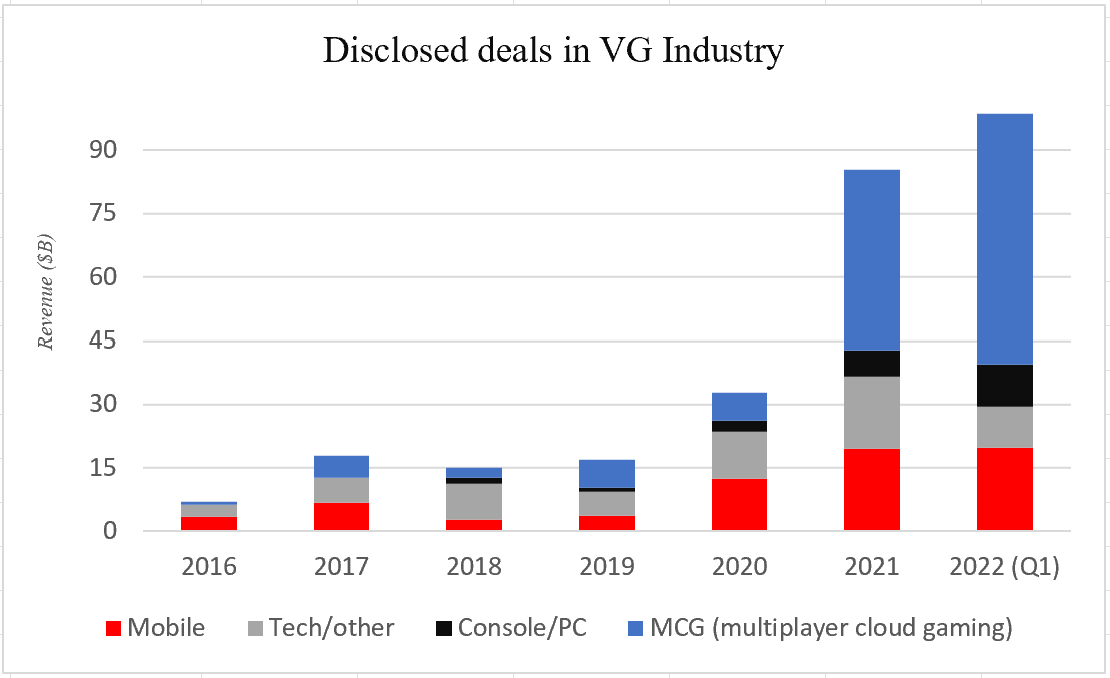

In Q1 2022, there was an acceleration of the acquisition practice with many billion value deals. Consolidation in the industry attained $98.7b (for 387 trans), which is more than what was done in the entire 2021 year ($85.4b for 1,159 deals), which was already almost the triple that in 2020 ($32.7B and 505 deals).

Source: DDM Games Investment Review (2022)

This is due to the biggest deals in the industry taking place right now. Microsoft acquired Activision Blizzard for $68.7b (owning Call of Duty, Wow, and Destiny), becoming the biggest acquisition in Video Gaming, just followed by the also 2022 Take-Two Interactive’s acquisition of Zynga for $12.7b (leader in the mobile entertainment industry). Sony Interactive Entertainment as well acquired Bungie for $3.6b (creator of the destiny franchise).

With an estimated market of $200b by the end of 2022, companies are fiercely competing to get a part of this growing cake. This also means the deal's value in Q1 is already half the revenue it should generate this year. It indicates an ongoing concentration of a reduced number of actors getting bigger and bigger market share. The market today is pretty fragmented, but we can easily imagine an Oligopoly in some 2 to 3 years at the rate it is evolving.

Source: T4.ai (2019)