Inflation: The Basics

Most A Level Economics students will have been taught that inflation is the enemy of money – a vulture eroding precious earnings, making economic agents worse off. Although that can be true, low and steady inflation is often an auspicious indicator of a healthy economy and welfare can actually improve despite its presence. Its importance and relevance has been apparent throughout the development of economics and financial markets, from the first appearance of market bubbles such as the Tulip mania and the South Sea Bubble; hyperinflation in Germany in the late 1920’s; a stagflating world economy in the 1980’s; and house price inflation foreshadowing the financial crisis.

But What Exactly Is Inflation?

Inflation is best described as the rate of change of prices from one period to another. This ‘basket’ of prices could be prices of consumer goods, shown by the Consumer Price Index (CPI) index and its predecessor, the Retail Price Index (RPI). Conversely, rates of house price changes are shown in the UK House Price Index and other asset price inflation can be shown via indexes such as the FTSE 100. Paul Davies of At Home Estate Agents and About Mortgages points out that whilst CPI inflation may impact house prices, there are other property related factors that have significant influence. "House price increases have far exceeded inflation in recent years. Policies such as the stamp duty holiday as well as demand factors have fuelled double digit house price increases for the year up to July 2022." The UK House Price Index calculated that house prices had increased by 15.5% during 2022 through to July.

Typically, the de facto gauge of price changes is consumer price indexes given that they are more representative than other indexes; for example, real estate and equities are often owned by those with significant wealth – although recent stock market news has highlighted the changing composition of wealth owners, with the introduction of more equitable brokerages leading to increased opportunity to purchase stocks for those who normally lack the requirements to open trading accounts. Despite that, CPI is often representative of the average household’s economic activity, and its figures are released on a monthly basis, and compared to previous months and years in order to gauge macroeconomic health.

Any positive rate of change is inflation, with a falling (but still positive) rate of change known as disinflation. Negative rates of change are known as deflation and high levels of inflation are known as hyperinflation, as seen in the Weimar Republic and most recently in Venezuela. The inflation rate itself is determined by the intersection of aggregate supply and aggregate demand in the macroeconomy, as provided below. Dynamics of these can determine inflation movements in either direction.

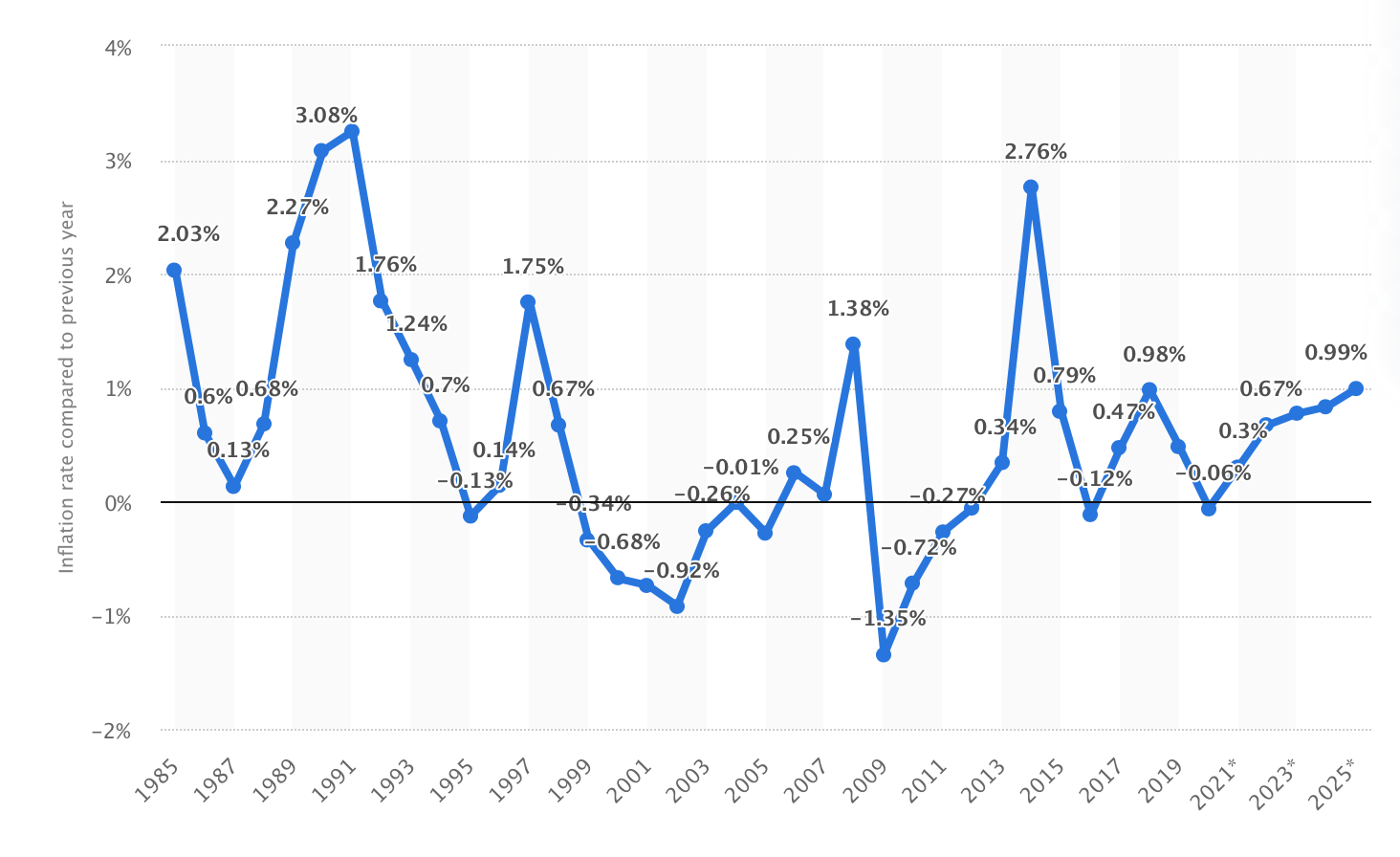

The UK’s most recent CPI figures are also shown below:

As one can see, inflation levels have fallen significantly during the pandemic, indicative of the contractionary environment from a growth perspective and well below the Bank of England’s target of 2% – low and stable inflation at the 2% level is indicative of a healthy UK economy.

Mathematical Definition

Given that changes in prices are discrete, the equation for the inflation rate is discernible from a given price index, such that:

The rate of inflation is the percentage change in the price index. The index itself has a base period of 100, for example, in the above CPI figures from the ONS 2015 is used as the base period. Therefore, figures for the CPI index will change if the base period is changed – it is all about relativity.

Times of Hyperinflation and Deflation

Ever since humanity has operated under a monetary system, inflation has been present in some shape or form. But there have been key periods in contemporary economic history when inflation has damaged the broader macroeconomy. The most famous case is most likely in Weimar Germany in the 1920’s when workers’ earnings were virtually wiped out in an immutable hyper inflationary spiral [3]. Real earnings can be expressed as nominal wages divided by the price level:

And hence the change in real wages is:

With the change in prices incredibly large, German workers experienced a constant erosion of wage income, leaving most worse off.

The beginning of the Iran-Iraq War in 1980 led to a huge spike in the price of oil, in turn fueling inflation across the world economy. By this point, globalisation had become the consensus: oil from OPEC states was being exported to developed countries to help drive guzzling 4×4’s and produce plastics for an increasingly consumerist society. This era was defined as stagflation, leading to the breakdown of the pre-eminent use of the Phillips Curve, which stated an inverse causal link between unemployment and inflation. Reagan and Thatcher then created the Monetarist paradigm, supported by proponent economists such as Milton Friedman.

Conversely, deflationary forces have made their way into the developed world in recent years. Evident in Japan since the 1990’s and with the developed world experiencing what some are calling “Japanification”, deflation looks like it can be beneficial from a return and growth perspective, but is more so indicative of a reluctant consumer and lack of growth, considering consumption is often a large component of GDP. Despite a strong reponse to inflation in the form of fiscal stimulus and yield curve control, Japanese inflation has not been above 3% since the late 80’s and is projected to stay below 1% until 2025, having shown deflation during the earlier part of the 21st century (below).

Inflation and Financial Markets

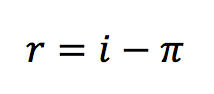

Inflation itself is a key variable in financial market dynamics, predominantly dictating movements in fixed income and gold markets. Given the nominal interest rate on a bond, the real interest rate is shown by:

That is, inflation erodes the real return of fixed income instruments. Given in recent months that the real return has become negative – and with inflation expected to return – gold has rallied since the onset of the pandemic, mostly due to hedging strategies, but also because its real return is zero: logic would guide investors towards it in times of inflation. Inflation also erodes the return of longer-dated bonds, leading to a selloff and steepening of the yield curve. A key barometer for this is the spread between the 2- and 10-year Treasury bonds, as shown below, this has increased by around ten basis points since the start of the year due to President Biden’s prospective $1.9 trillion stimulus package, yet to pass through Congress – this is known as the reflation trade. But given the decades-long bond rally and talk of “lower-for-longer” yields [5] – with central banks not looking to decrease the pace of QE measures and the possible experimenting of yield curve control – nominal yields are likely to stay at current levels for the time being.

Are We Measuring It Correctly?

One key question to consider is whether inflation is being measured correctly. We saw that consumer price levels in the developed world were fairly low in the buildup of the financial crisis, with globalisation being a deflationary measure from a supply chain and hence consumer good perspective. However, house price inflation was evident and ultimately acted as a harbinger of financial collapse – interest rates were therefore argued to have been too low in the years preceding the crisis. Therefore, with house prices still high and growing, as well as the argument of a stock market bubble occurring, are policymakers measuring inflation correctly, given consumer prices remain below target rates? Although the pandemic’s economic wreckage makes the question difficult, policymakers could place more emphasis on house price and asset price inflation when incorporating inflation into rate-setting models [7]. This is particularly pertinent given the increased access to real estate and stocks via the Help to Buy scheme and increased equity regarding stock market access via brokerages such as Robinhood.